BROWSE BY TOPIC

- Bad Brokers

- Compliance Concepts

- Investor Protection

- Investments - Unsuitable

- Investments - Strategies

- Investments - Private

- Features/Scandals

- Companies

- Technology/Internet

- Rules & Regulations

- Crimes

- Investments

- Bad Advisors

- Boiler Rooms

- Hirings/Transitions

- Terminations/Cost Cutting

- Regulators

- Wall Street News

- General News

- Donald Trump & Co.

- Lawsuits/Arbitrations

- Regulatory Sanctions

- Big Banks

- People

TRENDING TAGS

Stories of Interest

- Sarah ten Siethoff is New Associate Director of SEC Investment Management Rulemaking Office

- Catherine Keating Appointed CEO of BNY Mellon Wealth Management

- Credit Suisse to Pay $47Mn to Resolve DOJ Asia Probe

- SEC Chair Clayton Goes 'Hat in Hand' Before Congress on 2019 Budget Request

- SEC's Opening Remarks to the Elder Justice Coordinating Council

- Massachusetts Jury Convicts CA Attorney of Securities Fraud

- Deutsche Bank Says 3 Senior Investment Bankers to Leave Firm

- World’s Biggest Hedge Fund Reportedly ‘Bearish On Financial Assets’

- SEC Fines Constant Contact, Popular Email Marketer, for Overstating Subscriber Numbers

- SocGen Agrees to Pay $1.3 Billion to End Libya, Libor Probes

- Cryptocurrency Exchange Bitfinex Briefly Halts Trading After Cyber Attack

- SEC Names Valerie Szczepanik Senior Advisor for Digital Assets and Innovation

- SEC Modernizes Delivery of Fund Reports, Seeks Public Feedback on Improving Fund Disclosure

- NYSE Says SEC Plan to Limit Exchange Rebates Would Hurt Investors

- Deutsche Bank faces another challenge with Fed stress test

- Former JPMorgan Broker Files racial discrimination suit against company

- $3.3Mn Winning Bid for Lunch with Warren Buffett

- Julie Erhardt is SEC's New Acting Chief Risk Officer

- Chyhe Becker is SEC's New Acting Chief Economist, Acting Director of Economic and Risk Analysis Division

- Getting a Handle on Virtual Currencies - FINRA

ABOUT FINANCIALISH

We seek to provide information, insights and direction that may enable the Financial Community to effectively and efficiently operate in a regulatory risk-free environment by curating content from all over the web.

Stay Informed with the latest fanancialish news.

SUBSCRIBE FOR

NEWSLETTERS & ALERTS

FOLLOW US

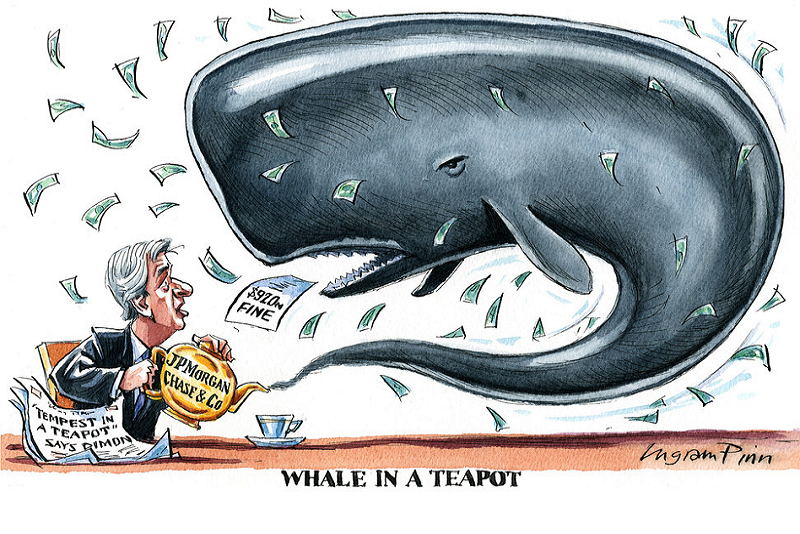

‘Justice’ Prevails in JPMorgan ‘London Whale’ Case

[Image: London Whale, by Ingram Pinn /lexicon/ft.com]

by Howard Haykin

Federal prosecutors dismissed charges against 2 ex-JPMorgan traders who supposedly played instrumental roles in the 2012 “London Whale” trading scandal by hiding billions in trading losses. The scandal ultimately cost the JPMorgan upwards of $7.2 billion, including $6.2 billion in trading losses. While the criminal case was closed, SEC civil charges are still pending.

The government’s case against traders Javier Martin-Artajo and Julien Grout depended in large part on testimony that would be provided by Bruno Iksil, who was dubbed the “London Whale – a name he got because of his outsized derivatives trades made while working in JPMorgan’s Chief Investment Office (‘CIO’) in London. Mr. Iksil agreed in 2013 to testify as a cooperating witness against his former co-workers.

However, in the intervening years, Iksil’s views have changed, leading the Department of Justice to issue the following statement: “Based on a review of recent statements and writings made by Iksil, however, the government no longer believes that it can rely on the testimony of Iksil in prosecuting this case.” Those statements and writings, which shifted responsibility to JPMorgan senior management, include the following:

- A February 2016 letter released to the media, in which Iksil said he had been "instructed repeatedly" by senior management in the CIO to execute the trading strategy that caused the losses.

- A website created by Iksil that provides his account of the “London Whale” case. [LondonWhaleMarionette]

- A 400-page unpublished memoir that would cast doubt on the core of the DOJ’s case.

HOW JUSTICE PLAYS OUT. Going back to the days when I published www.Compliance-Insights.com, I have always maintained that the London Whale scandal was simply too big a transaction for a couple of JPMorgan traders to hide or cover up. Others had to be in on the deal - including senior management, who no doubt gave their approval for the CIO to hold the positions in hope that the market would reverse an unprofitable position.

Here's my reasoning:

- Chairman and CEO Jamie Dimon was a hands-on executive who demanded to know every major trading position and transaction – particularly when JPMorgan had billions at risk. That was certainly the case with the derivative positions that the London Whale had accumulated. It was in 2012 that I wrote that Dimon and his knew about the credit default swap trades earlier than they were to admit. And Jamie Dimon's justification for giving CIO the go ahead to hold the position – i.e., not wind it down – was based pm his confidence in the Bruno Iksil, the London Whale (who was a highly regarded trader) and Ina Drew, who headed the CIO (when Drew retired/resigned 4 days after the trading loss came to light, Dimon heaped praise on Drew and promptly arranged for her to receive a generous retirement payout).

► Jamie Dimon sort of “tipped his hat” about his awareness of the trading losses in early 2012. When Q1 earnings were announced, reports began to circulate about a large trading loss, which prompted questions about the bank's risk management controls and Dimon's leadership. Dimon responded by dismissing the matter as a “tempest in a teapot” – though 4 weeks later he disclosed a $2 billion trading loss that could grow to $3 billion or more. Obviously, he didn't learn about the trading losses from the media.

► And yes, the losses subsequently ballooned while the bank first maintained, then carefully liquidated, its positions. Initially unbeknownst to anyone at JPM, a consortium of hedge fund insiders, led by Boaz Weinstein of Saba Capital Management, had figured out JPMorgan’s trading strategies positions and accumulated offsetting positions to squeeze the bank until it’s losses morphed into $6.2 billion.

- Bruno Iksil, in his memoirs, suggested that senior management at JPMorgan was fully aware of the issues - noting that even as losses mounted in 2012, valuations of those positions were communicated to top bank officers.

- A report issued by the U.S. Senate Permanent Subcommittee on Investigations concluded the bank didn’t express a problem with how the positions were being treated, brushed off internal warnings and misled regulators and investors about the scope of its losses. The same report, citing testimony from Mr. Iksil, stated that a decision was first made in 2010 to shrink the positions but didn’t attribute that order to any specific person.

- An internal investigation by JPMorgan - separate and apart from investigations conducted by U.S. regulators - that was published in January 2013 was quite critical of senior management, including Jamie Dimon. Among other things, the report criticized Dimon, former CFO Doug Braunstein and CIP head Ina Drew for inadequately supervising the traders. [However, this doesn’t address senior management’s role in managing the positions after they likely were informed of the market exposures.] [See Financialish: “Dimon & London Whale: Internal Report is Critical”]

- In mid-2012, former JPMorgan executives said they were troubled by assertions – or revelations – that London-based traders in the CIO may have intentionally mismarked trades in order to mask the size of trading losses. These individuals with direct knowledge of the unit’s operation said it made little sense - in part, for the following mark-to-market controls:

► JPMorgan required traders to mark their positions daily so the firm can track their profits, losses and risk. An internal control group double-checked the marks against market prices monthly and at the end of each quarter, said 3 former CIO executives and a senior executive in market risk. The firm uses the control group’s prices, not what individual traders submit, to calculate earnings, making it difficult for one trader or trading desk to rig prices, they said. [See Financialish: “Blaming JPM Traders Is 'Off the Mark' - Ex-Employees”]

Note: To access earlier 2017 Financialish stories about the JPMorgan London Whale, click on:

The JPMorgan London Whale Resurfaces [3/15/17]

Related Stories: Crimes

-

Like Money Flying Out the Window at Royal Alliance

April 15, 2020 -

Power of Attorney = Power to Convert

April 12, 2020 -

The Betting Line – ‘Zero Pay Off’ On a Sports Betting Scam

January 2, 2020