BROWSE BY TOPIC

- Bad Brokers

- Compliance Concepts

- Investor Protection

- Investments - Unsuitable

- Investments - Strategies

- Investments - Private

- Features/Scandals

- Companies

- Technology/Internet

- Rules & Regulations

- Crimes

- Investments

- Bad Advisors

- Boiler Rooms

- Hirings/Transitions

- Terminations/Cost Cutting

- Regulators

- Wall Street News

- General News

- Donald Trump & Co.

- Lawsuits/Arbitrations

- Regulatory Sanctions

- Big Banks

- People

TRENDING TAGS

Stories of Interest

- Sarah ten Siethoff is New Associate Director of SEC Investment Management Rulemaking Office

- Catherine Keating Appointed CEO of BNY Mellon Wealth Management

- Credit Suisse to Pay $47Mn to Resolve DOJ Asia Probe

- SEC Chair Clayton Goes 'Hat in Hand' Before Congress on 2019 Budget Request

- SEC's Opening Remarks to the Elder Justice Coordinating Council

- Massachusetts Jury Convicts CA Attorney of Securities Fraud

- Deutsche Bank Says 3 Senior Investment Bankers to Leave Firm

- World’s Biggest Hedge Fund Reportedly ‘Bearish On Financial Assets’

- SEC Fines Constant Contact, Popular Email Marketer, for Overstating Subscriber Numbers

- SocGen Agrees to Pay $1.3 Billion to End Libya, Libor Probes

- Cryptocurrency Exchange Bitfinex Briefly Halts Trading After Cyber Attack

- SEC Names Valerie Szczepanik Senior Advisor for Digital Assets and Innovation

- SEC Modernizes Delivery of Fund Reports, Seeks Public Feedback on Improving Fund Disclosure

- NYSE Says SEC Plan to Limit Exchange Rebates Would Hurt Investors

- Deutsche Bank faces another challenge with Fed stress test

- Former JPMorgan Broker Files racial discrimination suit against company

- $3.3Mn Winning Bid for Lunch with Warren Buffett

- Julie Erhardt is SEC's New Acting Chief Risk Officer

- Chyhe Becker is SEC's New Acting Chief Economist, Acting Director of Economic and Risk Analysis Division

- Getting a Handle on Virtual Currencies - FINRA

ABOUT FINANCIALISH

We seek to provide information, insights and direction that may enable the Financial Community to effectively and efficiently operate in a regulatory risk-free environment by curating content from all over the web.

Stay Informed with the latest fanancialish news.

SUBSCRIBE FOR

NEWSLETTERS & ALERTS

FOLLOW US

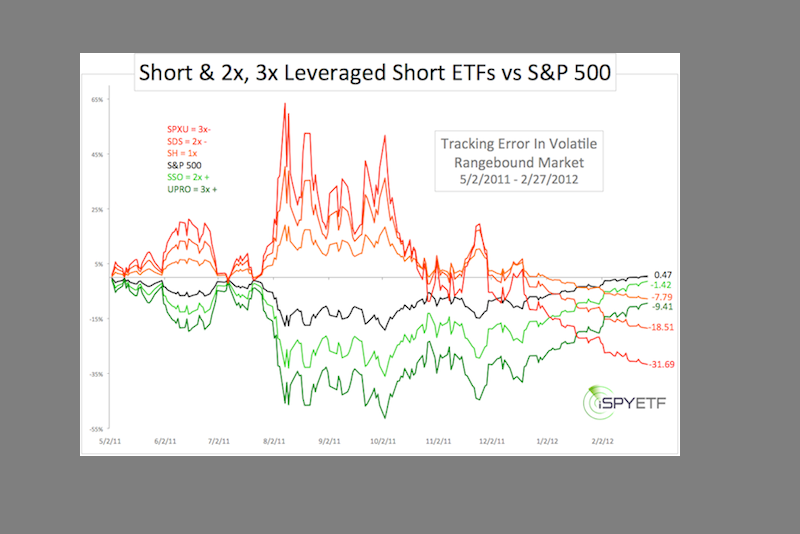

Lure of Leveraged Exchange Traded Notes Tripped Up Young Broker

[Image: Leveraged ETF - ispyetf.com]

by Howard Haykin

Todd Jones agreed to a $15K fine and a 4-month suspension to settle FINRA charges that he exercised discretion in client accounts without written permission to do so.

BACKGROUND. Jones, a resident of Shoreline, WA, has 4 years’ experience with 3 firms. He’s not been associated with a broker-dealer since being U5’d by JPMorgan in September 2015.

FINRA FINDINGS. On July 6th and 7th 2015, Jones exercised discretion to purchase nearly $210,000 of VelocityShares 3x Long Crude Oil (UWTI) in the accounts of 12 firm clients. None of the 12 clients, however, had provided Jones with written permission to exercise discretion in their brokerage accounts.

JPMorgan’s policies only permitted the purchase in brokerage accounts of leveraged exchange-traded products such as UWTI on an unsolicited basis. Jones marked most of the July 2015 UWTI purchases as unsolicited. When initially questioned by the firm, Jones claimed incorrectly that the trades were unsolicited; he later admitted that they were not unsolicited.

- ERROR #1. VelocityShares 3x Long Crude Oil were probably not suitable for Jones’ retail customers. They’re too speculative, and this relatively inexperienced broker probably didn’t understand the intricacies of this leveraged exchange-traded product.

- ERROR #2. Without having his customers’ expressed permission to purchase these leveraged ETN’s, Jones violated NASD rule 2510(b), which in relevant part states that…

"No . . . registered representative shall exercise any discretionary power in a customer's account unless such customer has given prior written authorization to a stated individual or individuals and the account has been accepted by the member. . ."

- ERROR #3. Jones mismarked most of the trades as “unsolicited” because JPMorgan restricted the purchase of leveraged ETNs to unsolicited trades. Maybe trades in one or 2 accounts could have passed as ‘unsolicited’ – but in 12 accounts? Near impossible.

FINANCIALISH TAKE AWAYS. It’s unfortunate that FINRA provides so little information about this case beyond the basic facts. With what we know, some valuable lessons or take-aways are lost. For example:

- Why did it take 2-1/2 months to complete its investigation or review of the trades (July 6-7 to September 22)?

- Who raised suspicions about the transactions - JPMorgan or FINRA?

- Were the leveraged ETNs purchased as long-term investments in the customers’ accounts?

- Were the trades reversed and, if so, were customers made whole for any losses?

- Had Jones discussed UWTI’s with his customers? Had he obtained their verbal ‘okay’ to purchase the securities?

Part of my thinking is ... now that broker-dealers have begun to enable their customers to trade in bitcoins, how long will it take FINRA to provide guidance and direction for its member firms? And will we encounter the same issues encountered years ago with leveraged exchange-traded products?

This case was reported in FINRA Disciplinary Actions for November 2017.

For details on this case, go to ... FINRA Disciplinary Actions Online, and refer to Case #2015047381301.